Social Security Tax Strategies

The Strategies listed are designed to provide a tax benefit today while meeting future financial goals such as Retirement, Emergency Fund and/or Legacy planning. By simply moving certain taxable assets into tax-advantaged accounts the interest earned does not appear on your tax return and is not used in calculating your combined provisional income. Combined Provisional Income is used to determine the taxable amount of Social Security Benefits. (The following illustrations and examples are conceptual only. Please contact us to have illustrations customized and tailored to your financial situation)

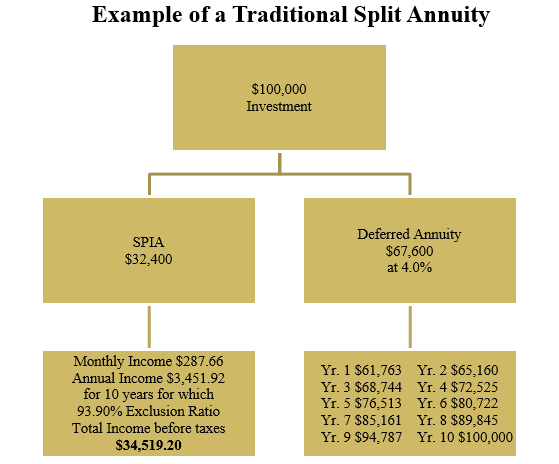

Retirement Strategy

An effective way to reduce the amount of income below the thresholds at which Social Security is taxable is to us a Non-Qualified Split-Annuity Concept. A Non-Qualified Split-Annuity concept can work well for someone who is spending the taxable interest income generated by their investments (CD's, Savings, Dividends, etc.) The Non-Qualified Split-Annuity Concept uses a Single Premium Immediate Annuity to create income now and a Fixed Deferred Annuity to re-accumulate the portion that has been used for income. The benefit of structuring money this way is how the income is treated for tax purposes. The Immediate Annuity provides Tax-Advantaged Income: Since a significant portion of your monthly income from the Immediate Annuity is considered a return of your original investment, it is not taxable. Therefore you pay less in taxes. The Deferred Annuity portion of the split-annuity offers tax-deferred growth and you earn an interest rate that historically has been higher than average CD rates. The general idea is to restore the original principal at the end of the guaranteed period, which allows you to start the process over again at prevailing interest rates

Legacy Strategy

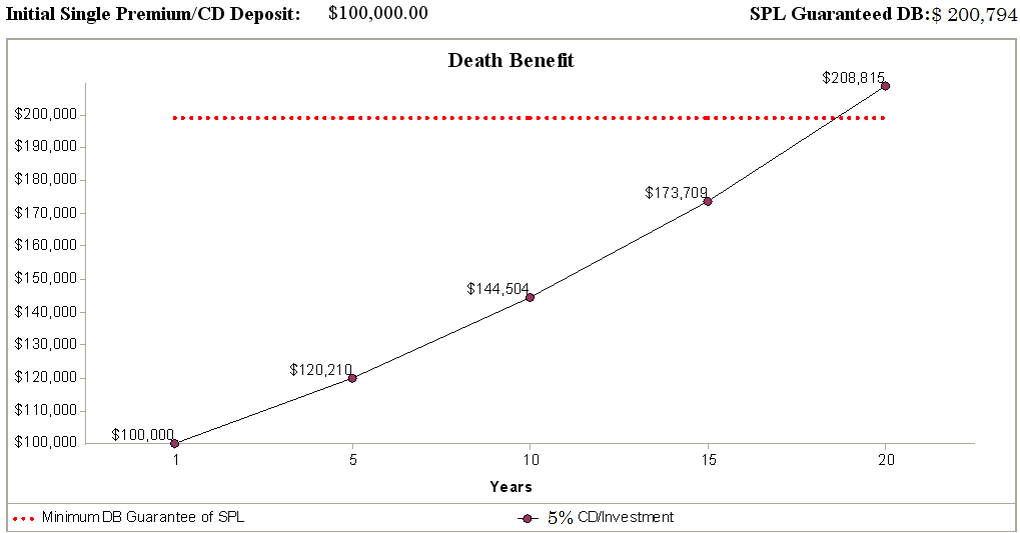

If you have determined you have money causing an increase in taxes and it’s not needed for living expenses. One of the most tax-efficient ways to transfer this money to your beneficiary is to use the account to purchase a permanent life insurance policy i.e. (Single Premium Life, Universal Life or Whole Life). Assuming you are insurable, one of the best ways to get the largest death benefit is to structure the account as a Single Premium Immediate Annuity; the income that is generated can be used to pay for a permanent life insurance policy. By structuring the account this way, the income is guaranteed to last for the life of the account owner and the tax can be stretched out over the life of the account owner. At the time of death the beneficiary receives the larger life insurance death benefit, free of estate and income tax. This Strategy also works with IRAs:

![]()

Strategy for Emergency Fund & Beneficiary

A Single Premium Life Contract can be used to reduce or eliminate the tax on social security benefits and is an effective way to satisfy the objectives of saving money for an emergency and passing a larger benefit to beneficiaries. This alternative tax-advantaged account provides tax deferral, safety and immediate liquidity. It has the same tax provisions for partial withdrawals as annuities but when it passes to a beneficiary upon the death of the owner, there is a major difference. The entire tax-deferred accumulation passes income tax-free to the named beneficiary.

Roth IRA Conversion

Contributing to a Roth IRA or Converting from a Traditional IRA to Roth IRA can potentially reduce or eliminate the tax on Social Security in later years. Income from a Roth IRA is tax-free and is not used in the formula to determine the taxable portion of Social Security. (Note: when converting to a Roth IRA the taxes are owed in the year of the conversion.)